Summary

A recent review of 2025 Form 10-K filings points to a higher bar for public-company disclosure. The biggest shifts this reporting season were in AI, tariffs and trade exposure, income tax transparency, and sustainability, with companies moving away from generic discussion and toward more direct explanations of financial and operational impact.

Key Highlights for Finance Functions

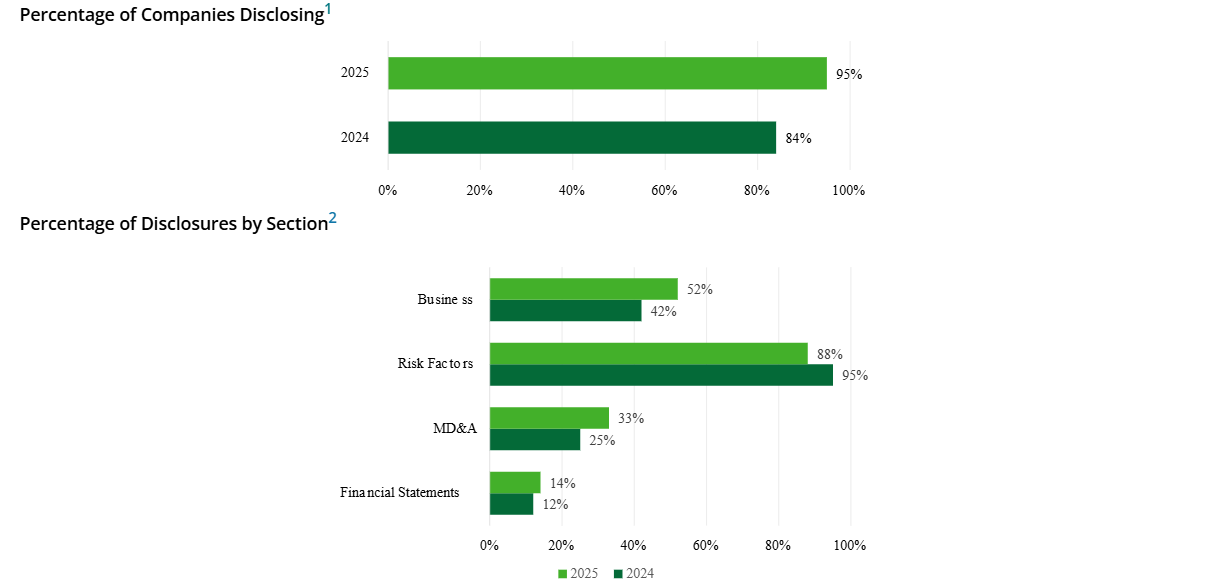

AI disclosure is getting more specific

Companies are moving beyond broad references to AI and instead describing use cases, governance, compliance, cyber risk, workforce implications, and expected business impact. For finance teams, this raises the importance of ensuring these disclosures are supportable and consistent with internal budgets, forecasts, and board reporting.

AI-Disclosure Trends Across Companies:

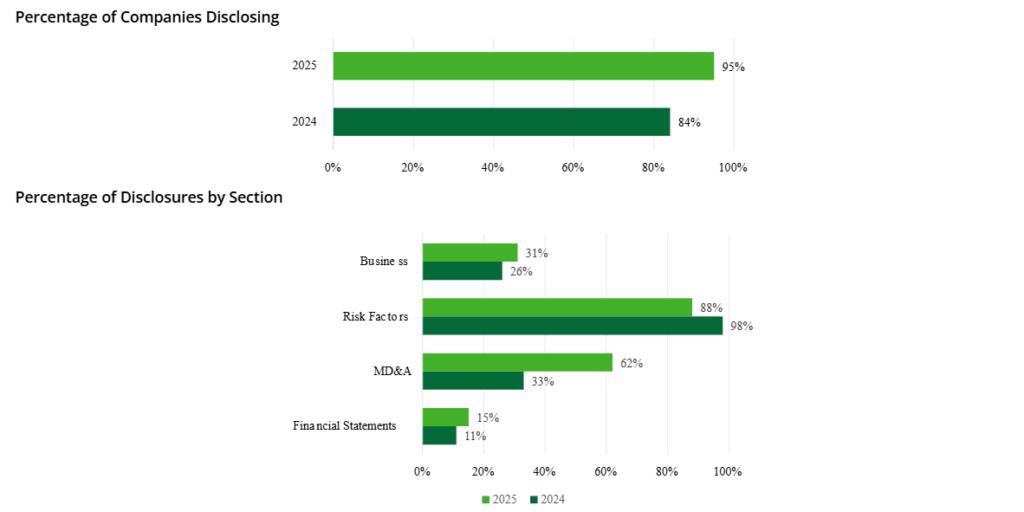

Tariff exposure is showing up more often in MD&A

Trade and tariff discussion is moving beyond standard risk-factor language and into management’s discussion of margins, sourcing, pricing, liquidity, and potential knock-on effects such as impairment or credit considerations. This shift suggests companies are treating tariff exposure as an operating issue, not just a macro risk.

Tariff-Disclosure Trends Across Companies:

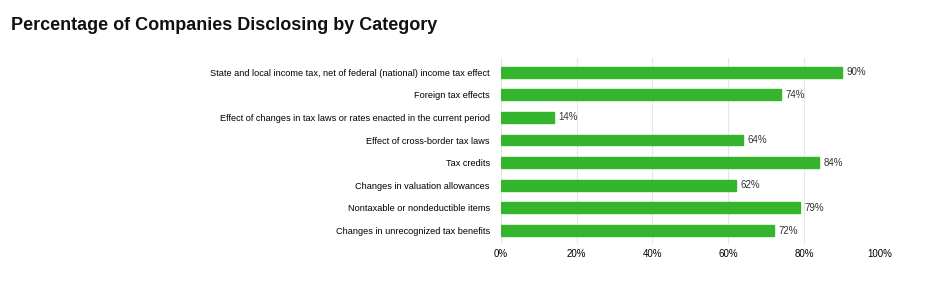

Tax disclosures are becoming more granular

The first year of implementation for the expanded income tax disclosure rules (ASU 2023-09) is making tax footnotes more detailed, particularly around rate reconciliation and jurisdictional taxes paid. As a result, tax profiles, geographic exposure, and cash tax trends are becoming easier for investors to evaluate. The chart below illustrates the number of filers that disclosed the respective categories within their income tax footnote.

Tax-Disclosure Trends Across Companies:

ASU 2023-09 also requires expanded disclosure related to state and local income tax jurisdictions. California was the most frequently mentioned state jurisdiction within income tax disclosures, with approximately 58 percent of companies referring to it, followed by Illinois (40 percent), New York (37 percent), and New Jersey (25 percent). The most frequently mentioned foreign jurisdictions were Canada (33 percent), United Kingdom (29 percent), Germany (21 percent), Mexico (19 percent), India (18 percent), and Brazil (18 percent).

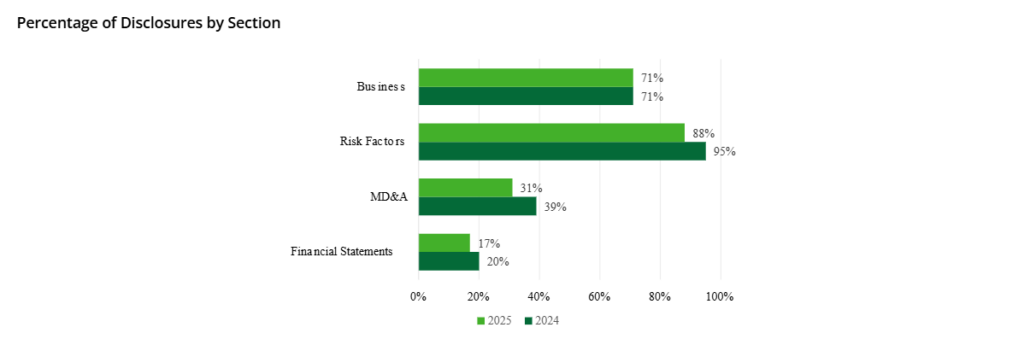

Sustainability disclosure remains part of core reporting

Despite evolving regulatory requirements, climate- and sustainability-related disclosures continue to appear broadly in annual reports. Such language is often communicated through existing SEC disclosure channels such as risk factors, business disclosures, and MD&A rather than as a standalone reporting framework. The practical emphasis is increasingly on business impact rather than policy language.

Sustainability-Disclosure Trends Across Companies:

Why it Matters to Finance

Finance leaders should expect continued pressure for disclosures that are specific, internally consistent, and tied to actual business consequences. That means validating AI-related statements against operating plans, refreshing MD&A for tariff and supply-chain effects where material, ensuring tax footnotes are ready for greater scrutiny, and aligning sustainability language with capital allocation, risk management, and strategy.

It also means disclosure preparation is becoming more cross-functional. Finance, tax, legal, investor relations, treasury, and operating leadership need to be working from the same fact base so that emerging-topic disclosures are precise and defensible.

Source note: This publication is informed by and includes data from Deloitte’s Disclosure Trends From the 2025 Reporting Season.

How Virtas Can Help:

Virtas helps finance and accounting teams navigate complex technical accounting, SEC reporting, and financial reporting matters with confidence. We work alongside management to assess, document, and communicate the accounting and disclosure implications of significant transactions, new standards, and evolving regulatory expectations.

Our professionals provide support with:

- U.S. GAAP and SEC reporting requirements

- Complex transaction accounting, including acquisitions, divestitures, carve-outs, and public company readiness

- Close and reporting deadline support

- Disclosure enhancement, internal controls, and compliance risk mitigation

- Practical insight to enhance readiness for transactions and investor engagement

For situations requiring rapid or targeted support, our On Call Accounting Solution provides direct access to Virtas professionals as an extension of your finance function.

You can contact Virtas Partners here.